Canadian Mortgage trends (THIS YEAR'S CMT MUSIC) provides the latest news about the mortgage in Canada for homes online mortgage brokers and real estate professionals. Legal information: consult a qualified Mortgage Adviser before making any mortgage decision, on the basis of the information, read here. Similarly, if you see a financial or tax strategy, discussed here, please consult a licensed and qualified investments or tax advisor to ensure that the strategy is right for you. Mortgages, investments, and tax strategies mentioned in this Web site are not suitable for all. In many cases, they may not ever be feasible or lead to serious risks. While reasonable efforts to ensure the accuracy of the information and data contained herein, accuracy, suitability, completeness, and facts cannot be guaranteed. Past performance is not good prognozator for future results. Results, percentages, strategies and conditions are not guaranteed, and THIS YEAR'S CMT MUSIC and associated takes no responsibility for any losses which may arise from your use of this information. The information on this site reflect purely our opinions and not necessarily the opinions of any other party. Readers are welcome to add comments. However, comments that are off topic, quarrelsome, accusatory without evidence, the hated Spanish insensitive, profane, libelous, misleading, made under different names by the same IP address, or otherwise rude, or is deemed inappropriate from THIS YEAR'S CMT MUSIC, can be removed without notice. THIS YEAR'S CMT MUSIC news site and is not related to most of the people or companies. Company logos and trademarks shown here are the property of their respective owners, are displayed only for comment, are not intended to be used in a competitive way with the owner and should not imply an association or affiliation between THIS YEAR'S CMT MUSIC and said brand owner or its products or services. Information here is not intended to be nor represent him, mortgage advice, investment advice, tax advice, financial advice, recommendations or have indicated for the purchase or sale of securities. THIS YEAR'S CMT MUSIC personnel and affiliates may have an interest in mortgages, services, companies, products or securities on this site. Contact us if you require clarification of the above. THIS YEAR'S CMT MUSIC is owned and operated by McLister enterprises Inc. For questions about the news to see here, mortgages, copyrights, or republishing'S CMT MUSIC content, contact us at (800) 280-2460 or info@canadianmortgagetrends.com. Thank you for reading THIS YEAR'S CMT MUSIC. Copyright 2010. All rights are reserved.

miércoles, 18 de mayo de 2011

MBS REMINDER: 5/18/2011

Afternoon Market Updates

There was a larger than expected slowdown in 1st quarter growth, but the Fed believes those effects will prove "transitory" assuming continued improvement in household balance sheets, easing credit conditions, and strengthening labor markets. The economy appears to be gaining enough traction to support a MODEST recovery, but remains highly sensitive to a number of variables including a larger-than-expected drag on household and business spending from higher energy prices, continued fiscal strains in Europe, larger-than-anticipated effects from supply disruptions in the aftermath of the disaster in Japan, continuing fiscal adjustments at all levels of government in the United States, financial disruptions that would be associated with a failure to increase the federal debt limit, and the possibility that the economic weakness in the first quarter was signaling less underlying momentum going forward. If the variables listed above do not slow the pace of economic expansion and growth resumes as anticipated in the second half of 2012, the Fed will likely be forced to begin the exit process from extremely accommodative policy. In preparation for such a scenario, the Fed economic staff gave a presentation on strategies for normalizing the stance and conduct of monetary policy over time as the economy strengthens. This does not mean the move toward such normalization would necessarily begin soon, but it does describe the steps the Fed will take toward tightening in the context of the economic outlook and the Committee's policy objectives.

As is more often the case for Thursdays than any other day of the week, tomorrow's calendar is thick with a variety of economic events. As always, you can get a detailed view of those with the link at the bottom of this update. Here's a snapshot: In terms of scheduled economic reports, Jobless Claims is the sole occupant of the 830am time slot. After that, there's a 10am triple-team with Existing Home Sales, Philly Fed Survey, and LEI. Of those, we'd tend to be most interested in Philly Fed although Tuesday's Housing Starts did illicit a bit of a market reaction, so perhaps tomorrow's Home Sales data will emulate. Whatever the case, 10am is packed. Fed speakers appear throughout the day as well with Dudley at 830am, Dudley at noon (yes, again), and Evans at 140pm. Also, though it's not nearly the same sort of market mover as a pure 10yr TSY note auction, there will be a 10yr TIPS auction tomorrow at 1pm which has a bit of market moving potential on occasion. 2 hours earlier, the next round of TSY supply is announced, though there isn't as much speculation of a reduction in offering sizes as there was 2 weeks ago.

Here is an excerpt from the FOMC Minutes discussing the state of the U.S. housing market: "Activity in the housing market remained very weak, as the large overhang of foreclosed and distressed properties continued to restrain new construction. Starts and permits of new single-family homes inched down, on net, in February and March, and they have been essentially flat since around the middle of last year. Demand for housing also continued to be depressed. Sales of new and existing homes moved lower, on net, in February and March, while measures of home prices slid further in February. Rates on conforming fixed-rate residential mortgages rose modestly during the intermeeting period, and their spreads relative to 10-year Treasury yields narrowed slightly. Mortgage refinancing activity remained near its lowest level in more than two years. The Treasury Department's announcement in late March that it would begin selling its holdings of agency MBS at a gradual pace had little lasting effect on MBS spreads. The Federal Reserve began competitive sales of the non-agency residential MBS held by Maiden Lane II LLC; initial sales met with strong demand, but market prices of non-agency residential MBS were reportedly little changed overall. The rates of serious delinquencies for subprime and prime mortgages were nearly unchanged but remained at elevated levels. However, the rate of new delinquencies on prime mortgages declined further."

Despite MBS having fallen more than enough to justify reprices for the worse, that hasn't been a widespread phenomenon as yet. That's not to say that they're not on the way, simply that lenders appear to be absorbing a higher than average amount of price losses in MBS. To quantify the weakness, FNCL 4.5's are down 8 ticks at 103-08 and 10yr note yields are up just over 6 bps on the day at 3.173.

WASHINGTON – The Consumer Financial Protection Bureau (CFPB) today announced the Know Before You Owe project, an effort to combine two federally required mortgage disclosures into a single, simpler form that makes the costs and risks of the loan clear and allows consumers to comparison shop for the best offer. Tomorrow, the CFPB will begin testing two alternate prototype forms that are designed to be given to consumers who have just applied for a mortgage loan. This testing – which will take place over the next several months and involve one-on-one interviews with consumers, lenders, and brokers. To view the combined forms and share feedback, check out this post: http://www.mortgagenewsdaily.com/05182011_gfe_til_combined.asp

With just over 40 minutes to go until the FOMC Minutes, a persistently bullish stock market is coinciding with persistent weakness for bond markets. It all speaks to the on again, off again possibility/fear that the current pace of the economic recovery is overdone. Traders may find clues that could help in deciding that in the upcoming FOMC Minutes. FNCL 4.5's are currently down 4 ticks on the day at 103-13 and 10yr notes are 4.6 bps higher in yield at 3.1599 near their weakest levels of the day. Several reprices for the worse have been reported since last update, and that risk remains for lenders who have not yet released one.

FNCL 4.5's have hit their lows for the 4th time today, down 6 ticks at 103-10. 10yr benchmarks just broke through their supportive ceiling at their highest yields of the day moving from 3.153 to 3.156. Reprices for the worse have been seen, and any lender that hasn't put one out yet is a risk, though the earlier rate sheets more so.

With the exception of 1 hour so far this morning, profit taking has been the order of the day, meaning that accounts are selling open fixed income positions, bringing prices lower and yields higher. The pace has been aggressive relative to recent instances of profit taking and without new short positions coming into the market, the selling pressure seems as if it has run its course for the morning. That leaves 10yr yields having bounced around 3.15 and stabilizing around 3.145. FNCL 4.5 MBS are down 4 ticks on the day at 101-12, the level that had previously served as 2011's bullish resistance (much like 3.14 had been in the 2011 resistance zone for 10yr notes). Best case scenario, if the rally continues, these could both turn out to look like great pivot points for the next leg lower in yield. But we wouldn't make any bets on that happening today unless the post-FOMC-Minutes trading is bond-bullish. With MBS near their lows of the day, we're still at risk of reprices for the worse, though with slightly less certainty than if we had moved straight down through the 103-12 zone.

Featured Market Discussion

Matthew Graham : "FYI, if anyone is looking for a recap of the pertinent points from the FOMC minutes shortly following the release itself, we will normally put those right in the chat window and make them "featured comments" so that if you click to view featured comments only, they should be easy to find and see beginning just after 2pm. "

Jill Statz : "my rep just told me that adding or removing a borrower is now standard FNMA policy now for DURP"

Matthew Graham : "seems that way so far"

Gus Floropoulos : "glad I locked this morning"

Matthew Graham : "10yr notes back at high yields. MBS at lows."

Michael Tadros : "Jill - I believe Flagstar sent out an update a few days ago that lets you restructure the note "

Victor Burek : "or death"

Victor Burek : "i thought you could if a divorce"

Jill Statz : "on a DURP loan you can not remove a borrower at all can you?"

Steve Chizmadia : "Agreed CK, It would have been nice on the sample forms though if they used an ARM example with adjustments and caps that actually existed."

Chris Kopec : "I've reviewed the forms....they are fine. Best we could expect, and much better than the crap sandwich we are currently forced to provide. I assume originator compensation will continue to be offset by lender credit, but I'll wait for further direction from our Federal Overlords on that."

Steve Chizmadia : "I was under the impression there will be a seperate page that discloses "commission""

Caroline Roy : "hi all, on the new combined GFE/ TIL form it would appear that there is no place for the YSP/credit? does that mean that the last two years of complaining about it worked?"

Adam Quinones : "FOMC Minutes: http://federalreserve.gov/newsevents/press/monetary/20110518a.htm"

Matthew Graham : "* A FEW SAW RISE IN INFLATION RISKS SUGGESTING FED MIGHT NEED TO TIGHTEN SOONER THAN CURRENTLY ANTICIPATED"

Matthew Graham : "* A FEW FELT FED SHOULD BE READY THIS YEAR TO TAKE STEPS TOWARD TIGHTER POLICY, POSSIBLY RAISING RATES OR SELLING ASSETS"

Matthew Graham : "* MOST SAW RISKS TO GROWTH OUTLOOK AS BALANCED, BUT A NUMBER SAW RISKS TILTED TO DOWNSIDE DUE TO ENERGY COSTS, EUROPE STRAINS "

Matthew Graham : "* MANY PARTICIPANTS HAD BECOME MORE CONCERNED ABOUT UPSIDE RISKS TO THE INFLATION OUTLOOK - FED "

Matthew Graham : "* FED PARTICIPANTS REVISED UP INFLATION PROJECTIONS FOR 2011, BUT SAW RECENT RISE IN INFLATION AS TRANSITORY "

Matthew Graham : "* FED - PARTICIPANTS VIEWED WEAKNESS IN Q1 GROWTH AS LARGELY TRANSITORY, BUT EVENTUAL PICKUP IN GROWTH SEEN LIMITED"

Matthew Graham : "* SOME PREFERRED THAT MONETARY POLICY OPERATE THROUGH A CORRIDOR SYSTEM WITH FED FUNDS IN MIDDLE OF RANGE-FED "

Matthew Graham : "* MOST SAW CHANGES IN FED FUNDS RATE AS PREFERRED ACTIVE TOOL FOR TIGHTENING MONETARY POLICY WHEN APPROPRIATE-FED "

Matthew Graham : "* A FEW PREFERRED SALES BEFORE RAISING RATES, A FEW PREFERRED RATE HIKES, ASSET SALES AT SAME TIME-FED "

Matthew Graham : "* GRADUAL SALES PACE BEGUN LATER SEEN ALLOWING EARLIER RISE IN RATES FROM ZERO; ALLOWS OPTION TO CUT RATES LATER IF NEEDED "

Matthew Graham : "* MAJORITY PREFERRED SALES OF AGENCIES TO COME AFTER FIRST INTEREST RATE INCREASE, MANY PREFERRED GRADUAL SALES PACE-FED "

Matthew Graham : "* FED-MOST FELT THAT, WHEN APPROPRIATE, ASSET SALES SHOULD FOLLOW PREDETERMINED, PREANNOUNCED PATH, BUT PATH COULD BE ADJUSTED "

Matthew Graham : "* CHANGES IN STATEMENT LANGUAGE REGARDING FORWARD GUIDANCE WOULD NEED TO ACCOMPANY NORMALIZATION PROCESS - FED "

Matthew Graham : "* FED -NEARLY ALL AGREED FIRST STEP WOULD BE CEASING TO REINVEST AGENCIES, AND SIMULTANEOUSLY OR SOON THEREAFTER, TREASURIES "

Matthew Graham : "* SALES OF AGENCY SECURITIES WILL BE COMMUNICATED TO PUBLIC IN ADVANCE, PACE ADJUSTABLE TO CHANGES IN CONDITIONS - FED "

Matthew Graham : "* OVER INTERMEDIATE TERM, FED WILL SHRINK BALANCE SHEET, RETURN TO HOLDING ESSENTIALLY ONLY TREASURIES - FED "

Matthew Graham : "* DISCUSSION OF NORMALIZATION STEPS DID NOT MEAN MOVE TOWARD NORMALIZATION WOULD BEGIN ANY TIME SOON - FED "

Matthew Graham : "* FED DISCUSSED SCENARIOS FOR NORMALIZATION OF POLICY AT APRIL 26-27 MEETING- MINUTES "

Adam Quinones : "you know best Terry. Pls share feedback on the post itself. The CFPB will be reading it."

Terry Colabrese : "AQ, I just looked over the link you posted. It's a little hard to think about this from the consumer's viewpoint, but: in what ways is this change making it more simple for the borrower to comprehend this information?"

Victor Burek : "nexbank worse"

Matt Hodges : "ty mbsonmnd"

Matt Hodges : "locked one with WF 1 hour ago"

Matt Hodges : "WF rep 1:01"

Andrew Horowitz : "-13/32nds yield at 3.16 a bit of perspective when referring to this "massive" sell off"

Jason Zimmer : "i was fine with the switch from the old gfe to new because it was a new concept, but to just tweek and cause all this mess all over again is really frustrating"

Steven Bote : "I do see all that, VB, and I get what you all are saying. With this version, it basically makes it so that I will have to explain the difference between closing costs, and total setttlement costs. Which is by the way, what I have to do now with the current version of the GFE and TIL."

Victor Burek : "bote... you are looking at the same form... it says A+B+Cetc = total closing costs.,not total settlement costs"

Victor Burek : "how many clients will say... you are chargine me $10000 in closing costs... no mr. client..good portion of that is escrow..."

Victor Burek : "all those are not closing costs...insurance and escrow is not a closing cost...it is a settlement cost.... the form should be accurate"

Steven Bote : "It spells it out right there, A+B+C, etcetera = total settlement costs."

Steven Bote : "You should be able to explain that to your clients, VB."

Victor Burek : "i dont like line F...should say total settlement charges..not total closing costs"

Ira Selwin : "They are looking for feedback VB, theres a bunch of info on the site "

Victor Burek : "so that form is supposed to take the place of gfe and til?"

Ira Selwin : "Sample 2: http://www.consumerfinance.gov/wp-content/uploads/2011/05/disclosure2.pdf"

martes, 17 de mayo de 2011

Get the home page of the collection is on loan to a credit limit check is not in the United Kingdom

- Get door-to-door loan- picture adfunk"

A collection of home loans are available without credit scoring up to £ 500. Even if you have a poor credit history loan, home sales in the ordinary course of business, can help you.

When does not have a bank account or credit history up poor, collected in mortgage loans to provide an alternative way to deal with forgery of money and with borrowing. Home sales, mortgage companies offer personal service, where you can get to work with a local agent, instead of the faceless telephone Center.

These lenders to help people who have been rejected in the rest of the credit, but they come under the supervision of the Office of Fair Trading (OFT). Ray Watson, OFT Director of consumer credit, group says, "we are working to improve the practices of the industry to protect the sensitive consumers."

How much money you can borrow from the lender, home sales?

The people who need fast money do not need to pass the credit check box. It does not matter if you are in breach of the recent credit agreements, you will still be able to borrow up to £ 500 for the period up to 52 weeks. Contrast this to when the loan is usually at least four wheels and a maximum term of one calendar month of small loan funds.

Once you've demonstrated that you have a reliable customer, you can even read bad credit of £ sales cash loan. Repayments can still better for 108 weeks. Many customers have the opportunity to develop excellent relations with their home loan sales.

What is the cost of the loans households collected in the United Kingdom?

This article in respect of the Daily Telegraph on 10 October 2008, is called "the high cost of home loans, sales", Kara is "Gammel Provident financial lends money to a door-to-door people with poor credit, explains its customers that if they lend £ 300ne would cost more than £ 504 56 weeksthe annual percentage rate of charge, is 183pc. "

From the beginning of the credit for the cost of the downturn has continued to increase. For example, the £ 300 to more than 33 weeks Greenwood personal credit loans cost you door-to-door, £ 495. The annual percentage rate of charge is 433.4%. You can compare the cash assets of the exchange rates compared to the loan, the lenders, the independent price comparison website.

The advantages and disadvantages of home sales, cash loans

Domestic sales of the cash loan could help to address the economic, as a matter of urgency, such as the repairing your vehicle, so that you can get to work. It is, however, are not suitable for poor credit rating to borrow money for frivolous purposes. It is important to remember that you can have tomorrow's cash today effectively costs.

A collection of home loans is useful for people who need quick money, but they do not come cheap. Adverse credit-lending and money is a risky proposition-the client, so you expect the interest rate should be paid to the Kingdom. This will reduce the disposable income, until you've borrowed money has been paid in full.

lunes, 16 de mayo de 2011

Q&A with FICOM CEO Caroline Rogers

Recently we had the chance to run a few questions by Carolyn Rogers, CEO and Superintendent of financial institutions Commission (FICOM), BC. mortgage broker regulator.

Rogers shares his perspective on issues such as obligations of mortgage brokers, reciprocal provincial licensing and areas to be aware of where the brokering online.

This discussion is here:

THIS YEAR'S CMT MUSIC: as mortgage brokers more business with customers via the Internet, issues, what does this increase the FICOM?

CR: obviously the Internet provides an effective communication channel to the public through the Internet brokers can emit rates, mortgage information and advice and the provision of online mortgage applications. However, there are several challenges which it presents to the Internet:

The use of the Internet increases the likelihood that brokers will have fewer meetings live. This can lead to brokers, costs less time advising borrowers on the details of the mortgage obligation or cost of credit disclosure.

It is useful for the broker to sit in front of a customer and review the documentation of important to them, highlighting the key components of the mortgage transaction as fees because, APR or cost of the credit calculation form for disclosure. Also the lack of direct interaction can lead to increased instances of title fraud and impersonation, if the broker finally does not satisfy the borrower to verify that they are dealing with.

In some cases, we found that mortgage brokers who work with customers electronically are also geographically remote from the property is mortgaged. They may therefore be familiar with some unique characteristics of the property, which can affect the value of the property and affect the lender.

As an example, there has not been a condominium complex in Vancouver, which is well known because of several news articles about used for marijuana grow operations. Local firms refused to deal with borrowers to finance these condominiums. However, geographically dispersed broker who relied on the Internet for customers, ruined financing for some of the owners of condominium and aware of their illegal use and potential problems of the State.

The increasing popularity of the Internet has also led to the spread of unregistered mortgage brokering activities. It is easy for illicit operators to create Web sites that offer mortgage financing to the public. In some cases, these web sites provide more detailed data for the operator and can be created for the purpose of carrying out the advance fee fraud with enticing high risk borrowers to pay an advance fee in return for the promise of fundingthat never materialized.

Some of the web site an unregistered activity may also provide that mortgage applications for receipt of financial information to sell to fraudsters for purposes of identity theft. Some of the Web sites may be misleading in that appear to work with mortgage originators with access to lenders, but in reality are the mortgage mortgage lead generators (which probably not registered) from different parts of the continent or the world.

Unbeknownst to the user, they will collect data for the application of the borrower to sell to third parties, which may include mortgage brokers or lenders. These mortgage brokers will use the acquired information to ask the user for the mortgage business. Many users have complained of our Office for this practice, leading to us issuing a newsletter, explains that the mortgage lead generators are involved in generating activities which require a mortgage broker registration.

THIS YEAR'S CMT MUSIC: what is the FICOM position of reciprocal mortgage agent licensing with other provinces (such as Ontario and Alberta). FICOM support this initiative?

CR: as a whole FICOM maintain reciprocity; However, this support should be made mainly with the removal of obstacles to the mobility of labour, instead of creating more competition between brokers and therefore better pricing to consumers. To our knowledge there is no lack of competition in the mortgage broker.

We have been cooperating with our neighbouring provincial regulators, the real estate Council of Alberta (RECA), for several years. There is one page of our Web site, which explains the requirements for becoming registered in British Colombia, with the help of a mortgage broker qualification of Alberta. There are similar reciprocal provisions for mortgage brokers of British Colombia who wish to obtain a broker in mortgages licensing in Alberta. British Colombia is also a party to the new partnership in the West and trade agreement with the Alberta and Saskatchewan, which will require a similar cooperation with Saskatchewan, from 1 July 2013. Discussions with the financial services Commission of Saskatchewan is expected to start later this year.

Finally, we are also on a case by case basis with licensed mortgage brokers in Ontario which are licensed with the financial services Commission of Ontario and who wish to obtain registration in British Colombia.

THIS YEAR'S CMT MUSIC: FICOM has specific regulations and guidelines which impose fiduciary duty on BC. mortgage brokers to recommend the most appropriate mortgage product, and to attempt to ensure the most competitive mortgage rates to their customers?

CR: law on mortgage brokers do not contain any specific requirements, requiring mortgage brokers to recommend the most appropriate mortgage product for the borrowers and the most competitive interest rates. This is not a simple matter, since some mortgage brokers also have mortgage lenders and administrators, or they actually represent the lenders, including the unsophisticated investors.

However, mortgage brokers are under an obligation in law to provide statements in advertising or other materials – so special equipment, if they argue, to find the best rates for borrowers ", and they do not, then they may be trained in the law on execution of false declarations or engaged in detriment of the behavior.

In addition, the common law of Agency, if the broker has created an agency relationship with the customer, they will have a fiduciary duty is owed by you to find the best speed of the most appropriate product for the customer.

And finally, all conflicts of interest must be clearly indicated to the customer in accordance with the requirements of the law. Any failure of a broker to disclose conflicts or to act in the interest of the borrower, while acting as a fiduciary may lead to disciplinary action by the Registrar.

Bar: for more information about adjusting the FICOM of BC. mortgage brokers see this link.

Rob McLister, THIS YEAR'S CMT MUSIC

MBS REMINDER: 5/16/2011

Afternoon Market Updates

NEW YORK, May 16 (Reuters) - U.S. Treasury yields have likely bottomed after the recent rout in commodity markets caused a safe-haven stampede into bonds, and will inch higher, a top bond fund manager at BlackRock said on Monday. Rick Rieder, who oversees half of BlackRock's $1.15 trillion of fixed-income assets, told Reuters that he will consider buying Treasuries if 10-year yields rose to the 3.60 to 3.75 percent range, 0.40 percentage point above their current level. "Now it's hard to see tremendous upside (on yields)," Rieder told Reuters of the Treasuries market. Rieder, who is chief investment officer for fixed income, fundamental portfolios, was reluctant to add risky debt securities ahead of the Federal Reserve completing its $600 billion bond buying program, dubbed QE2. BlackRock has been paring its holdings of the so-called non-agency mortgage bonds that had been rallying for nearly two years, he said. The outlook is short-term, however, as the firm's portfolios are expecting to resume its purchases at lower prices, Rieder said. "We've upgraded in quality in portfolios, increased liquidity in the instruments we hold in some of them, as you get closer to the end of QE2 on the assumption you get more volatility," he said. Separately, it would be tough for Treasury Inflation-Protected Securities to sustain their rally this year after the commodity sell-off and a fall in inflation expectations, Martin Hegarty, who co-heads the management of Blackrock's $22 billion in global inflation-linked portfolios, told Reuters. (Reporting by Richard Leong and Al Yoon, Editing by Chizu Nomiyama)

Two lawmakers have introduced bipartisan legislation that would eliminate Freddie Mac and Fannie Mae while still keeping a government presence in the housing finance marketplace. HR 1859, "The Housing Finance Reform Act of 2011", is sponsored by Congressmen Gary Peters (D-MI) and John Campbell (R-CA). Peters/Campbell have aimed this bill at overhauling the federal mortgage finance system and winding down the embattled mortgage giants, Fannie Mae and Freddie Mac, while establishing a new system of private mortgage associations - funded by private capital. Sponsor's believe the legislation will ensure liquidity in the secondary mortgage market because mortgage investments would still be backed by a government guarantee, which the plan has mandated strict standards around to safeguard taxpayers. In addition to these mandates, the legislation would extend current loan limits until Fannie and Freddie are no longer in conservatorship. FHFA has six months to provide a transition plan to wind down the GSEs and must determine within one year after five associations have been chartered whether the GSEs can be safely placed into receivership, an event that must occur no later than three years after two associations have been chartered.

In a break from a recent trend of "lower highs and higher lows," MBS are a few ticks better than their previous high, currently up 3 ticks on the day at 103-11. Reprices for the better are possible at these levels, and become increasingly likely the longer they hold or the greater margin by which they are surpassed.

In the course of the last two hours, 10yr yields improved 4 bps and FNCL 4.5's rose from 103-05 to 103-10 before running out of steam. 10's are currently at 3.1691 and 4.5's at 103-09. The joint movements are emblematic of markets that continue to bide their time, choosing to favor what has mostly been a consolidating range in the month of May. The resistance bounces for both MBS and TSYs fall in line to a series of slightly less ambitious resistance bounces. But the supportive levels have been getting higher and higher as well. This combines with the moving trend on the resistance side to suggest a consolidation centering on 3.20 in 10yr notes (roughly).

(Freddie Mac) -HomeSteps, the real estate sales unit of Freddie Mac, is launching a nationwide sales promotion for its inventory of foreclosed homes starting today. The HomeSteps Summer Sales Promotion is offering up to 3.5 percent buyer's closing cost and a $1,200 selling agent bonus for initial offers received between May 16, 2011 - July 31, 2011 and escrows are closed on or before September 30, 2011. This offer is valid only on HomeSteps homes sold to owner-occupant buyers. A two-year Home Protect® limited home warranty that covers electrical, plumbing, air conditioning, heating and other major systems and appliances is offered on some eligible HomeSteps homes. Home Protect also provides discounts of up to 30 percent on the purchase of appliances. (Terms, conditions and limitations apply. Not all homes or borrowers will qualify. For details, see www.HomeSteps.com/smartbuy.)

Rate sheets are about unchanged vs. indications on Friday when both reprices for the better and worse were reported in the same session. At the moment, risk is skewed toward the potential for unfavorable reprices, especially with rebate mostly flat and production MBS coupon prices moving marginally lower. Our negative reprice target is 103-02 in FNCL 4.5s. This would imply benchmark 10s were testing 3.21% support. Reprices for the better are more likely to be awarded as FNCL 4.5s move into positive territory and approach the 103-12 level. We currently do not recommend floating if you need to lock within the next week to 10 days.

(Freddie Mac) -In the first quarter of 2011, fixed-rate loans accounted for more than 95 percent of refinance loans, based on the Freddie Mac Quarterly Product Transition Report released today. Refinancing borrowers overwhelmingly chose fixed-rate loans, regardless of whether their original loan was an adjustable-rate mortgage (ARM) or a fixed-rate. An increasing share of refinancing borrowers chose to shorten their loan terms during the first quarter. Of borrowers who paid off a 30-year fixed-rate loan, 34 percent chose a 15- or 20-year loan, the highest such share since the first quarter of 2004. Eighty-four percent of borrowers who had a hybrid ARM chose to refinance into a fixed-rate product during the first quarter, continuing a pattern of the past few years of borrowers revealing a strong preference for fixed-rate over variable-pay contracts."The mortgage rate on 15-year fixed was about three-fourths percentage point below that on 30-year fixed during the first quarter. For borrowers motivated to refinance by low interest rates, they could obtain even lower rates by shortening their term. In the first quarter we saw the largest share of borrowers shortening their term while refinancing in seven years."

Featured Market Discussion

Matthew Graham : "S&P's heading into dangerous technical territory right now, and with only 12 official minutes left"

Matthew Graham : "there was talk before the last announcement that the 3yr offering size might be cut 1-3 bln, but that didn't transpire. I think it a near impossibility that any auctions would be postponed. More likely would be a VERY minor reduction in the offering size of the short end"

Chris Kopec : "Question: are auctions going to be postponed (i.e., 3, 5, 10 year auctions)? Or, are there other book-keeping manuevers that will clear more room for them."

Mike Drews : "Wells reprice"

Chris Kopec : "5/3 abd flagstar repriced"

Jill Statz : "PF another .125 for .25 better on the day"

Ira Selwin : "famc price change. We were owed that one"

Matthew Graham : ""jumping off" or "stepping off logically based on where they perceived the final destination of the bandwagon to be" "

Andrew Horowitz : "MG so blackrock is jumping off the bandwagon now"

Jill Statz : "Flagstar better"

Steve Chizmadia : "Mine is free standing, but there is no condo id to cross reference on VA approved condo list. I have confirmed with county they all have seperate apn's and legal descriptions, so I'm guessing VA should accept it, just wanted to confirm"

Steve Chizmadia : "Have any of you come across site condos on a VA loan? They are all individual units with no attached walls. I was under the impression that the HOA (there is none) and complex would not have to VA approved. Is this correct. I recently closed one on a FHA loan and wanted to know if any of you knew if VA followed the same "site condominium" guidelines"

Matt Hodges : "2 mos. reserves, 49.9% max dti"

Matt Hodges : "WF for us - we got a waiver last week"

Ken Crute : "what corr lenders are going to 620 on FHA?? "

Ira Selwin : "it's ok: These entities would not be allowed to discriminate against any originator, but the "Associations" could be formed for the general purposes of serving a particular mortgage market or category of mortgage lenders such as community banks. The legislation does allow banking organizations to acquire an interest in such categories of lenders"

Chris Kopec : "So instead of Fannie, we'll allow the mega-banks to be assigned even more institutional importance ...... someone tell Ozzie to stop the Crazy Train."

Chris Kopec : "Let;s replace Fannie - which was created in response to the last crash, and which functioned very well until it was warped beyond recognition by crony capitalism."

Andrew Horowitz : " An association can purchase a mortgage with an LTV higher than 80 percent if the seller retains a 10 percent stake in the loan, agrees to repurchase the mortgage on the demand of the association or private mortgage insurance is used to cover the balance of the loan above 80 percent. LOL"

Chris Kopec : "I have zero faith in GSE replacement."

Adam Quinones : "Bipartisian GSE Replacement Bill Takes Shape. Mirrors MBA Plan: http://www.mortgagenewsdaily.com/05162011_gse_reform.asp"

Jill Statz : "PF .125 better"

Adam Quinones : "not seeing much motivation in the market at the moment."

Jason York : "on fha, if there were lates, then it is like a foreclosure, if there were no lates, then there is no penalty, of course there are lender overlays though"

John Rodgers : "like a foreclosure on conv"

Steven Bote : "Anyone know how short sales on credit are viewed now for repeat buyers? I heard it's more or less treated just like a default with certain underwriters and so they can't qualify until four years from the deficiency?"

Housing prices, some, but not for a long period of weaker Sydney

- New Home Under Construction - Phil Keeffe

Sydney's property prices continue to soften, but there are underlying strengths in the market that should see a return to increases over the next six months

Recent house price figures from the Australian Bureau of Statistics indicate that most capital city property markets showed signs of slowing in the March quarter. The ABS reported that prices for established houses in Sydney fell by 1.8% during the March quarter, restricting the annual increase to just 0.8%.

Australian Property Monitors figures for the March quarter show a slightly lower rate of price weakening. APM says that Sydney median prices fell by 0.4% during the quarter. This statistical variation is understandable, given that APM and the ABS use slightly different methods of calculating the median price.

However, as usual with the Sydney market, not everything falls at the same rate. In fact, not all Sydney house prices are falling.

Writing on Domain.com, Dr Andrew Wilson noted that in the past year the top five suburbs in median house price growth were Kensington (30.9%), Westmead (30.7%), North Sydney (28.9%), Lewisham (26.1%), and Neutral Bay (25.2%).

Dr Wilson also notes that Sydney remains the most expensive capital city in which to buy a house or a unit. The March quarter Sydney median house price was $643,713, and for units the median price was $448,585.

So it follows that renting is more expensive in Sydney than any of the other capital cities. Figures from Australian Property Monitors says Sydney's March quarter median weekly asking house rental was $485 – 33% per cent higher than Melbourne's $360.

Dr Wilson leaves us in no doubt about the future of Sydney house prices: “Expect Sydney houses and units to remain prohibitively expensive compared with other capitals, particularly as it clearly has the best prospects of a sustained recovery in prices from the current subdued market conditions being experienced in all Australian capital city housing markets.”

Interest Rate Hikes Expected

There are signs that the Reserve Bank will be raising its interest rate in the near future. A report by Richard Gluyas in The Australian says that the head of the CBA Bank, Ralph Norris, expects “...one or two more increases in official interest rates in the next six months.”

The report also said that Mr Norris is optimistic about conditions between now and the end of the year.

“Notwithstanding present challenges, we continue to expect a gradual improvement in operating conditions through calendar 2011, as the economy recovery strengthens and system credit growth rebounds,” Mr Norris said.

Another sign of what lies ahead is the rising number of new homes sold, which increased for the third month in a row.

An AAP-sourced story in The Australian said that the latest Housing Industry Association (HIA) new home sales report showed the number of new homes sold across Australia increased by a seasonally adjusted 4.3% in March, following a 0.6% rise in February.

The article quoted HIA chief economist Harley Dale, who said there was still a long way to go for new home sales to reach healthy levels.

"The March result for new home sales reflects an ongoing pause in the interest rate hiking cycle and some abatement of the severe weather conditions witnessed in early 2011," Dr Dale said.

The HIA also noted that sales volumes remain low by historic standards, and that the level in March was nearly 1000 sales lower than the average over the past decade. It joined the CBA Bank in forecasting an interest rate rise on the horizon.

"However, it's now apparent that the next move from the Reserve Bank may be early in the third quarter of 2011, and this runs the risk of reversing the upward trend in sales," the report said.

The HIA report said that NSW new home sales were up by a "very encouraging" 13.5% in March, for a 20.7% rise in the first quarter of the year.

"Sales are on somewhat of a barnstorming run in NSW, from an awfully low base," the report said.

Which Way now for House Prices?

Domain.com’s Michael McNamara, a property commentator and valuer, tried to sort out the direction of house prices.

“At this stage, the indices show that home owners have simply given back the capital gains they have achieved over the preceding 3 quarters. In short, over the year, national house prices have recorded no meaningful change.”

McNamara notes that finance approvals (a forward indicator of buyer confidence) are declining while at the same time stock levels (properties on the market) have begun to increase.

He says that the number of properties advertised in Sydney (comparing March year on year) have risen from 42K to 46K, or about 9%, and asks whether this growth in supply will team with the fall in demand to further weaken prices.

His conclusion is that the shortfall in demand from the owner-occupier sector will be offset by growing demand for properties from investors.

“Landlords are rubbing their hands together over the last five years’ results; according to SQM research, rental values, in Sydney for example, have climbed at a compound rate of 8.5% per annum, clearly exacerbated by vacancy rates below 1.5%.”

McNamara says that a combination of excellent rental returns, a shortage of rental properties and steady employment levels will pull Sydney prices out of their decline over the next six months.

“Today, yields in Sydney are at 5.4% and rising. There is no glut of accommodation, no rising unemployment. Quite the opposite.”

Journalist Chris Zappone, writing in the Fairfax newspapers ‘Business Day’ column, says the federal government’s decision to lift "the overall increase in the permanent migrant intake to 185,000 from 168,700 places," will further strengthen demand.

He quotes St George chief economist Besa Deda who said that boosting immigration "...means more demand for housing and dwelling starts are failing to keep pace with population growth at the moment”.

Ms Deda told Zappone that even without the increase in skilled migration, dwelling starts won't catch up with population growth for some years and the housing shortage problem could likely continue.

Zappone commented that Australia now faces an estimated 200,000 shortfall of houses and apartments, with building approvals continuing at historically weak levels.

Negative Gearing to Stay

This ongoing shortfall in meeting demand for property has a silver lining for investors in that it supports the federal government’s favourable taxation policies for property investors.

Terry Ryder, in his ‘Hotspotting’ column in The Australian, strips away the props for all those advocating an end to negative gearing in the hope it can somehow improve housing affordability.

“There is a growing debate about the reasons for rising property prices, which in itself is rather odd because we all learnt the cause in high school economics. There is strong demand for a commodity that is in relatively short supply. It's that simple.”

He says that the economy is strong, unemployment is falling, wages are rising, Australia’s individual wealth is at record levels and personal debt levels are falling.

“The only outcome of stopping negative gearing will be to create a shortage of rental properties, which will force up rents and make it harder to first-home wannabes to save a deposit - that's what happened the last time it was scrapped.”

Ryder even sees the bright side of rising house prices: “This pattern of rising home values is a good thing for most Australians, because about 70% of households own their homes.

“It's also good for the nation because the value of the family home is the financial imperative by which many Australians fund their retirement.”

Sources

- ABS 6416.0 – ‘House Price Indexes: Eight Capital Cities, Mar 2011,’ 2 May 2011

- ‘Prices are falling - some suburbs still hot,’ Domain.com, 7 May 2011

- ‘A slight hiccup, but house prices still on the up,’ Sydney Morning Herald, 9 May 2011

- ‘CBA ready for two official rate rises in next six months: Ralph Norris,’ The Australian, 11 May 2011

- ‘New home sales on the rise,’ AAP report in The Australian, 5 May 2011

- ‘Rents underpin property values,’ Domain.com, 10 May 2011

- ‘Inflation, rates and a deep breath,’ Domain.com, 5 April 2011

- ‘HIA: Budget worsens housing affordability,’ Sydney Morning Herald, 11 May 2011

- ‘Scrapping negative gearing won't make housing more affordable,’ The Australian, 5 May 2011

domingo, 15 de mayo de 2011

Spring mortgage statement-CAAMP

Canadian Mortgage trends (THIS YEAR'S CMT MUSIC) provides the latest news about the mortgage in Canada for homes online mortgage brokers and real estate professionals. Legal information: consult a qualified Mortgage Adviser before making any mortgage decision, on the basis of the information, read here. Similarly, if you see a financial or tax strategy, discussed here, please consult a licensed and qualified investments or tax advisor to ensure that the strategy is right for you. Mortgages, investments, and tax strategies mentioned in this Web site are not suitable for all. In many cases, they may not ever be feasible or lead to serious risks. While reasonable efforts to ensure the accuracy of the information and data contained herein, accuracy, suitability, completeness, and facts cannot be guaranteed. Past performance is not good prognozator for future results. Results, percentages, strategies and conditions are not guaranteed, and THIS YEAR'S CMT MUSIC and associated takes no responsibility for any losses which may arise from your use of this information. The information on this site reflect purely our opinions and not necessarily the opinions of any other party. Readers are welcome to add comments. However, comments that are off topic, quarrelsome, accusatory without evidence, the hated Spanish insensitive, profane, libelous, misleading, made under different names by the same IP address, or otherwise rude, or is deemed inappropriate from THIS YEAR'S CMT MUSIC, can be removed without notice. THIS YEAR'S CMT MUSIC news site and is not related to most of the people or companies. Company logos and trademarks shown here are the property of their respective owners, are displayed only for comment, are not intended to be used in a competitive way with the owner and should not imply an association or affiliation between THIS YEAR'S CMT MUSIC and said brand owner or its products or services. Information here is not intended to be nor represent him, mortgage advice, investment advice, tax advice, financial advice, recommendations or have indicated for the purchase or sale of securities. THIS YEAR'S CMT MUSIC personnel and affiliates may have an interest in mortgages, services, companies, products or securities on this site. Contact us if you require clarification of the above. THIS YEAR'S CMT MUSIC is owned and operated by McLister enterprises Inc. For questions about the news to see here, mortgages, copyrights, or republishing'S CMT MUSIC content, contact us at (800) 280-2460 or info@canadianmortgagetrends.com. Thank you for reading THIS YEAR'S CMT MUSIC. Copyright 2010. All rights are reserved.

Interest mortgages: Hit Wall

Borrowing costs home loans have hit the wall.

The achievement of the best

levels of the year on Friday last week, the rate may not be able to

further improvement. That is not a bad thing because they clearly have not impaired either. Consumer rate quotes instead held tight to the top levels of the year. It reminds me of us quite a lot of early

March, during the closing costs having been stagnant for several days after the

quickly improve.

You will see "the wall", we have already hit in

This week updated chart that compares the origination costs

as a percentage of the amount of the loan for several available mortgage Note

rate. If the line is moving up, costs are getting more expensive for this

Special rates. If the line is moving down, costs are becoming cheaper.

Each row represents a different 30-year fixed rate mortgage Note.

The numbers on the right vertical axis are initiated as closing costs,

the percentage of the amount of the loan, the borrower will be required to pay

To close on the rate of this Note. If the line chart rates Note below

tag 0,00%, the consumer may potentially receive closing cost assistance from their

the lender in the form of loans lender. If the line rate of the Note is above

tag 0,00%, the consumer should expect to pay additional points on the

the closing table to buydown and origination fees. PLEASE SEE THE

OUR MORTGAGE RATES BELOW DISCLAIMER

The current market: "best execution" of conventional 30-year

mortgage rate is 4.75%. If you are looking to move down there,

You will evaluate the trade-offs between higher and lower the costs of closure

the monthly payments. This may be it is applicants who plan to

storing their new mortgage outstanding for sufficiently long to benefit on

the cost of additional upfront. For FHA/VA 30 year fixed "best execution"

It is 4.5%. 15 year fixed conventional loans are preferably priced at 4000%.

Five of the best are priced at 3.375% but market ARM is more stratified

i will be more changes in what will be the "Best-execution"

Depending on your individual scenario.

Previous guideline: And we'll keep a lock on the bias

for scenarios, Lock/float shorter time limit. You cannot lock on perfect

the day of the week, but will continue to be blocked during one of the better weeks

year. You're way ahead of the game. The Possibility Of

the intermediate to longer term rates Rally remains in the table.

Current orientation: WITH

a full week's worth of lender rate sheet information available on our chart

It is plain to see Why we need to continue to express the bias towards blocking. Although there is a possibility that we only detained and bok gone before the rates and the costs of further improvement, is not the highest probability

bring in the next week. It is more likely that costs will move

higher. Whether there is a temporary

fixed or is less certain, but as you can see at the beginning of March in today's

Chart, costs continue to worsen before eventually improve on the last occasion the main

before we hit like walls. From the point of view of the risk/reward,

the decision is clear for a shorter term perspective. Lock up 'em.

For those inclined float or have no other choice, the ability to

the intermediate to longer term rates Rally remains in the table. For more information:

Coercionmargin hits headlines. FALSE Start baked to bonds.

What should you consider before one thinks about writing on

the rate of the world?

1. What is NEEDED? Rates may not be as much as You Rally

want/need.

2. When YOU NEED IT by? Rates may not be as fast as you can Rally

want/need.

3. how to HANDLE STRESS? Whether you're ready to make difficult

decisions?

----------------------------

* "Best execution" is the most effective combination of Note

offered rates and points paid at closing. This rate is calculated on the basis of a Note

time required to recover the points paid child-resistant fastenings (rabat) vs.

monthly savings permanently purchase down mortgage rates by 0.125%.

When deciding whether to pay points, the borrower must have an idea

If you intend to maintain their mortgage. For more information, ask the

Outsourcer to explain the results of their "benefit analysis"

rate constants to buy lower cost.

Important: mortgage rate Disclaimer loan "best execution"

offers made available to the above are generally regarded as a more aggressive

primary mortgage. The originators of loans only will be able to offer these

rates for conforming loan amounts to highly qualified borrowers, who have

FICO score above 740 Center and sufficient equity in their home in order to qualify

refinance or large enough savings to cover down payments and closing

costs. If the conditions of your loan to trigger any risk based loans price level

the correction (LLPAs), quote the rates will be higher. If you do not belong to

Category "excellent borrower", make sure that asks the user for a loan

the principal for an explanation of the features that make it pay more

expensive. "No point" of the loan does not mean "no cost" loans. The

Best rates mortgages conventional/FHA/VA 30 year fixed still contain closing

such costs as: third party fees + title fee + transfer and recording. Not

forget frisking that comes with the tax from the insurance process.

miércoles, 11 de mayo de 2011

Young homeowners expected early debt freedom: poll

Call it the youthful ignorance or a genuine determination – a way young homeowners are expected to free yourself from the shackles of debt more quickly than their parents.

Study of the freedom of quarterly debt of the Bank of Manulife reveals that Canadian houses of more than four of 10 aged between 30 and 39 prediction of free debt until the end of their forties. Another third prediction, they will have their debts paid by their statutory rights.

Reality, however, paints a very different picture.

This disconnect between good intentions and also actually following their customs themselves manifest by mortgage advances. Flexibility of payment is one of the most sought-after mortgage functions. Still CAAMP 2010 annual survey found that only 12% of the mortgagors actually made a lump-sum payment of their mortgage over the previous year.

Despite the good intentions of many new housing Manulife President and CEO Doug Cognick noted that the plan on each product shall be subject to unexpected life events, such as home repairs, illness or job loss.

"Debt freedom is possible, but this requires a commitment to financial discipline and for many people, some tips on how to plan finances in the long term," he said.

The average homeowner, aged 30-39 is $ 209,200 in total debt, according to the survey. These in their statutory have an average of $ 108,500 for long.

Surprisingly, the survey showed that 19% of the homes in their statutory actually increased their debt in the last 12 months. Another sobering statistic in the poll is that 20% of the housing age 50-59, or unable to provide that, where they would be debt-free, or is not expected to ever reach that point.

Steve Huebl, THIS YEAR'S CMT MUSIC

MBS reminder: Reprices reported

Fehler beim Deserialisieren des Textkörpers der Antwortnachricht für Vorgang "Translate". Die maximale Länge für Zeichenfolgeninhalt (8192) wurde beim Lesen von XML-Daten überschritten. Dieses Kontingent kann durch Ändern der "MaxStringContentLength"-Eigenschaft des beim Erstellen des XML-Lesers verwendeten "XmlDictionaryReaderQuotas"-Objekts erhöht werden. Zeile 1, Position 10084.

Afternoon Market Updates

Moments after the 3pm official close, MBS and TSYs are well into their worst levels of the day. FNCL 4.5's are down 5 ticks on the day at 103-13 and 10yr notes are up to 3.202, a 4.5 basis point increase on the day. Lenders that haven't already repriced for the worse are now more likely to do so.

The slight bit of bearish bias in bond markets following the 3yr note auction just took another small and incremental into negative territory. The 10yr note is now just barely ABOVE 3.19 and FNCL 4.5's are at their lows of the day at 103-15. Loan pricing was mixed this AM. Some lenders owed gains from yesterday while others were flat on first release. With FNCL 4.5s -3/32 and 4.0s -6/32, reprices for the worse are possible from the lenders who withheld rebate yesterday afternoon. If your pricing was dinged this morning, you have a few more ticks to work with...if the downtrend continues you too are likely to see unfriendly recalls.

Despite a reasonably normal 3yr note auction bond markets first move following the auction was to their weakest levels of the day with FNCL 4.5's falling to 103-14 and 10yr notes getting almost as high at 3.19. But both have moderated somewhat with 4.5's currently at 103-16, and 10yr notes at 3.182. It's still a moving target however, and if we had to guess, we'd say it looks a bit more bearish than bullish as far as bonds are concerned. If 10's tick further back toward 3.19, or MBS back toward 103-14, reprices for the worse would become more likely.

* U.S. SELLS $32 BLN 3-YEAR NOTES AT HIGH YIELD 1.000 PCT, AWARDS 20.92 PCT OF BIDS AT HIGH *U.S. 3-YEAR NOTES BID-TO-COVER RATIO 3.29, NON-COMP BIDS $25.87 MLN * US TREASURY - PRIMARY DEALERS TAKE $16.60 BLN OF 3-YEAR NOTES SALE, INDIRECT $10.46 BLN

ARLINGTON, Va., May 10 (Reuters) -- The U.S. economic recovery is humming along despite high unemployment and depressed housing activity, making it key for Federal Reserve policymakers to remain vigilant about budding hints of inflation, Richmond Fed Bank President Jeffrey Lacker said on Tuesday.

Lacker said improved household and business spending, as well as strong exports led by demand from fast-growing emerging nations, was helping to support the economic recovery.

A self-described inflation hawk who is not a voter on this year’s Federal Open Market Committee said he expects energy prices to stabilize or ease a bit, allowing overall consumer price growth to trend back toward his preferred goal of around 1.5 percent.

"We should not take that outcome for granted, however. I would be concerned if I expected substantial further price increases, but at this point, futures markets are pricing in modest declines in petroleum products," Lacker told the Northern Virginia Regional Forum.

"Having said that, our experience over much of the last decade demonstrates that a flat futures curve does not preclude further price hikes." (Reporting by Pedro Nicolaci da Costa; Editing by Neil Stempleman)

10yr notes are effectively at their highs of 3.18 with just over 30 minutes to go before the 1pm 3yr note auction. FNCL 4.5's are slightly above their lows of the day currently 1 tick down versus yesterday at 103-17. This has also proven to be their preferred pivot point of the day with more touches here than anywhere else. Risks of negative reprices for the worse are somewhat elevated since we last updated you but are most likely to change (for better or worse) after we see how accounts bid for the lowest yielding 3yr in 4 months.

With the passing of this morning's data, we see that the week indeed looks to officially begin with the auction cycle. Volume is light and trading patterns are technical. The slightly higher yields than yesterday, consolidating around 3.17 suggest a bond market that's in the process of getting in position for today's auction. FNCL 4.5's are down a tick on the day at 103-17 and FNCL 4.0's are down 4 ticks at 100-10. The former is near previous lows while the latter is at the lowest level of the day. With 4.5's only down 3 ticks from peak to trough, it's not overly likely that we'll see reprices for the worse, but we're perhaps at the "early warning sign" stages.

Featured Market Discussion

Adam Quinones : "i need a shoe shine."

Mike Drews : "wf reprice"

Michael Tadros : "Sounds smarter than half the people selling the product"

John Rodgers : "My customers are soooo smart. After giving my client the caps on a 7 year ARM he responded with .................5% - 1st adjustment -> This is the maximum increase at year 7, which coincides with the total maximum lifetime increase over the 30 year loan period. Therefore the worst possible rate could be 9.125%

2% - subsequent adjustments -> This is the maximum increase at year 8 and after wards up to a maximum total increase of 9.125%.

5% - life cap -> Maximum cap at 9.125%.

Index – 1 yea"

Brent Borcherding : "Sierra Pacific worse .15"

Victor Burek : "5/3rd repriced for the worse"

Andy Pada : "Cash window at the GSEs only off by 4 or 5 bps."

Victor Burek : ".15 worse at flag"

Victor Burek : "flagstar worse"

Jill Statz : "PF .125 worse"

Brent Borcherding : "I locked 3 this morning, inside 30 days, I can renegotiate if necessary, but I believe there's greater risk of short term rise."

Shane : "MG & AQ - i just cancelled my subscription with one of your competitors (not sure if you would consider them a competitor or not tho)...now lets bring on 2.0!"

Adam Quinones : "quote " With 4.5's only down 3 ticks from peak to trough, it's not overly likely that we'll see reprices for the worse, but we're perhaps at the "early warning sign" stages.""

Matthew Graham : "benchmarks broke out of support, 4.5's and 4.0's hit lows of day, always going to be an "on toes" kinda time. "

Matt Hodges : "pricing likely occurred 3 tic higher and it looks like an ugly trend WC. If i were secondary, I'd want to get in front of it"

Adam Quinones : "just an early warning to be on your toes."

William Crawford : "We are only down 2 tics, why the negative reprice warning?"

Chip Harris : "The report we provided currently at this time is only designed to gather your client information and is not designed to be uploaded into the NMLS website at time. Unfortunately for now you will need to manually input the data into their site until future updates will allow for a xml upload."

Chip Harris : "Update on the Call Report from Calyx web support:"

Matthew Graham : "DEALERS SUBMITTED $25.66 BLN OF TREASURIES FOR CONSIDERATION IN FED PURCHASE -NY FED"

Matthew Graham : "FED BOUGHT $6.68 BILLION OF TREASURIES MATURING BETWEEN MAY 2015 AND SEPT 2016 -NY FED"

Get Cheap loans in the United Kingdom (English)

- Get a low interest rate loan picture vaclassialliberal"

Loans low interest rate level is the cheapest way to borrow money. Here is some advice, which will increase dramatically in the adoption of the probability.

If you prefer, you can get the approval of the loan, the interest is added to the Cheap may itself give final judgment in the lender's position. They want to profit, but the current economic climate, their priority is to get the money back. This means that they will only accept your application if you have a statistically less likely to be the default terms and conditions of the credit agreement.

With that in mind you will have to take measures to improve the credit rating. Income from debt is low, and you pay each time your punctually, so the more they want to you? No less evident are some of the factors that greatly increase your chances of getting the loan, the lowest rate accepted.

Improve your credit report (1)

Martin Lewis stated in this article, the MoneySavingExpert.com, called the "credit rating: how it works and improve it in the" a ":" Info in the report of the economic, to the other, whether the links are in the elections, roll, credit accounts, payments, or defaults to Miss onmitään and the other a list of your recent searches. "

The cheapest personal loans are offered only to persons who have an excellent credit history. Credit search does tell us that the information is to be kept about you by the lender is wrong. This applies even if you've always paid on time. If the information is incorrect, denied.

To order a copy of the statutory credit report-Equifax, Experian and call credit. Each report will pay £ 2, but if you held a 100% accurate. If it is not correct, follow the reference to each of the credit institution to the institution in accordance with the method described in this bug.

Low interest rate loans to existing customers

If you are connected to the good relations between the Bank, the possibilities are that you have already been approved in advance in the cheapest loans. Banks such as Barclays, HSBC and Santander, the pre-approve legitimate customers. Log in to Internet banking and see if you've been pre-approved.

Lowest APR loans are available to valued, long-term customers that a loan of more than £ model. This is because the lender receives more interest the service life of the loan. For example, the annual percentage rate of the loan is the HSBC 21.9%. However, if you borrow £ 7,250, you pay for the highly competitive 7,5%.

Find low loans comparison service

If you are not pre-approved, you still have the option. The comparison of the service, such as the uswitch or comparethemarket, should use the lowest interest rate for the pair trawl on the loans. All what you have to do is condition, and you can find the best peer to another, depending on the size of the banks and lenders offered loans interest rates.

Whenever you make an application for a credit search is performed, and this record, the reference to the credit protection for a period of 12 months. Too many applications in a relatively short period of time to hurt your chances to get approval. Do not use unless the eligibility criteria.

The Sources Of The

- Lewis, Martin. (12 April 2011). "The credit rating: how it works and it improves the". " MoneySavingExpert.com

lunes, 9 de mayo de 2011

MBS rally update: Paused moving "Down" in the coupon "

Not only is today silent partnership within the meaning of the trading volume, but there wasn't much direction in the charts on either. The ranges were narrow and only tightened as the day progressed. Short covering again was the main culprit for the lower yields TSY.

Here are a few charts ... ".

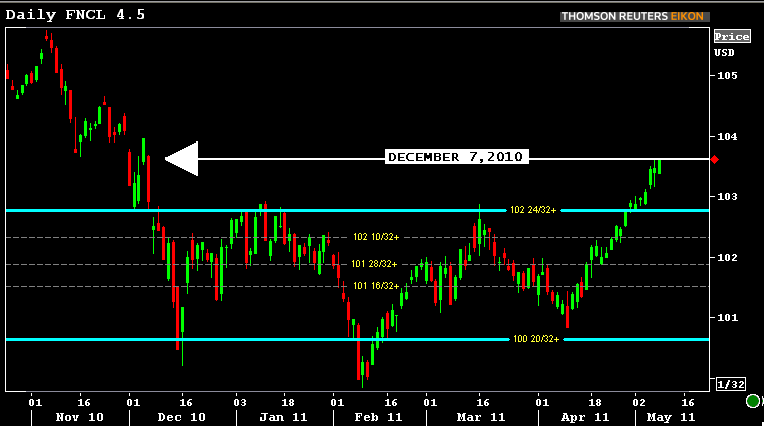

FNCL 4.5 is currently visiting levels not seen since 7 December 2010 FNCL 4.4S remain coupon production of choice for loan pipeline hedgers but shift "Down" in the coupon"is still in the infant stage. It seems as though real money accounts are taking routes "Cheapest to deliver and manage the duration of the interruption of mtg options contracts (CMM/CMS) while quick $ money managers are dabbling in coupons logarithmic as 4 0s and 3.3s.

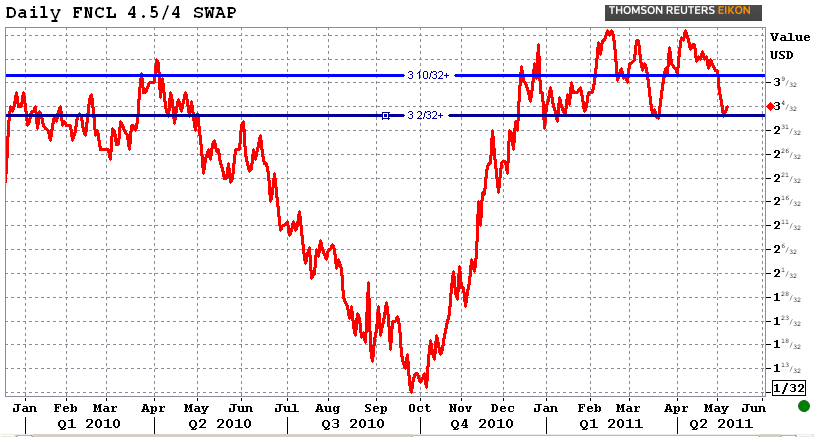

Replace the coupon FNCL 4.5/4 is a gauge of positive developments with regard to the willingness of the loan pipeline hedgers to move "Down" in the coupon ". I will look for an increase in the sale of loans 4.0 MBS (lock security desk) as the exchange of intercoupon 4.5/4 approach in 280/s wide. Currently Exchange FNCL 4.5/4 is activating around long-term resistance to 312/s.

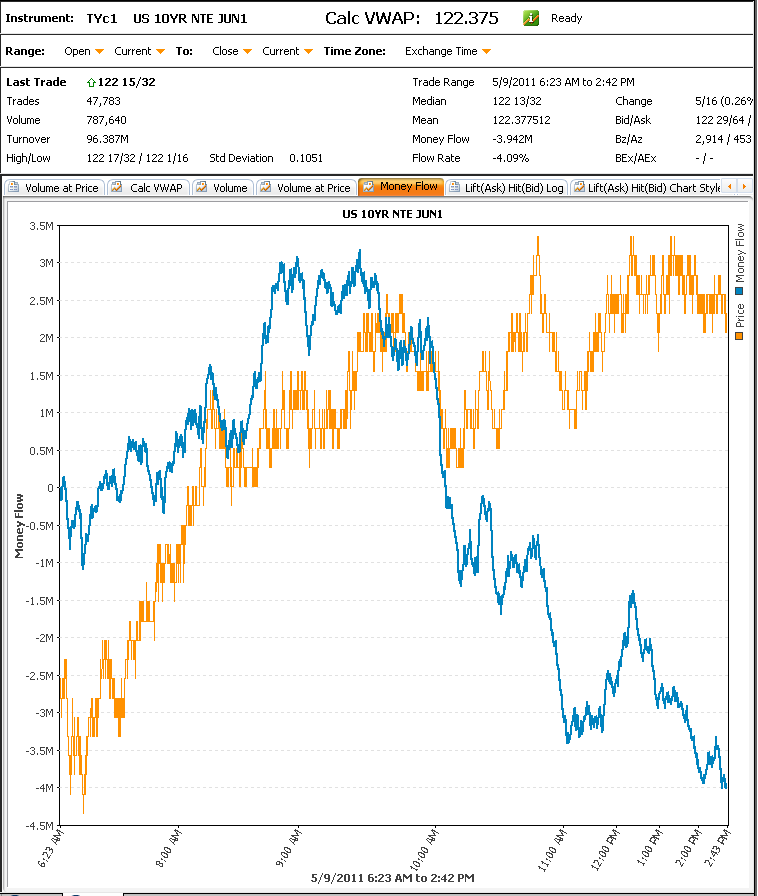

The chart below shows the cash flows in the TSY 10-yr futures contract. When prices go up and the flow of money fails, the prices of the shares is indicative for short.

Short covering the leading role in driving the current rates.

"Short covering" is at bearish trader closes positions, which was opened with the intent to have a lower price/performance.

The term "short," describes a trader directional bias. Simply "Including" shall mean confinement of an item. The resulting effect on short covering is in "open interest, which represents the number of open contracts on the market. If the operator has set up a short

location and prices continue to rise, and then their position is considered to be

be under water, or "red". Leaving open a short position as rates continue to Rally may be dangerous, because the location gets more expensive with each uptick in the price. So should be the sense that as rates continue to Rally it forced more covering of short, which led to the snowballing on the bond market. Forced covering short is a registered trademark of investors Waving white Flag on their bearish position but does not mean there are more rally to come. This behavior is to promote, especially when done in the matter, but must be intensified

by investors money (as opposed to quick $) need to move their funds "in the coupon". It must also be backed by the confirm weaker economic fundamentals and less protective gear.

Below is an updated version of our long term 10 yr TSY Note yield chart. I took the liberty of drawing a horizontal line at current levels to illustrate the past behavior of the market in a similar environment. As you can see 3.14% has a few drops of steep and profits surrounding it. This reflects the duration of the adjustments required by the fixed income managers cash flow as travel through this level of yield inflection.

We have three "suspects" lying in wait for the event tomorrow. A combination of economic data, Fed Speak and round the Treasury auction should be sufficient to shake things up a bit. In fact, each of the next days 3 contains all three of these participants, with Friday containing only econ data.

Tomorrow kicks off some early 730 am data in the form of the NFIB Small Business optimism Index.

In and of itself is not a significant part of the market mover, but you can add momentum if combined with similarly bearish or bullish ingredients which have been mixed session overnight. Prices hit on 830 m followed by wholesale trade for 10: 00. Do it for the econ data. Fed Speakers include Duke on 930 m and Lacker in 1245 pm 1 pm finally yields

What is potentially the largest moving day: auction TSY 3 years.

Give her a refund of taxes on your lender?

Canadian Mortgage trends (THIS YEAR'S CMT MUSIC) provides the latest news about the mortgage in Canada for homes online mortgage brokers and real estate professionals. Legal information: consult a qualified Mortgage Adviser before making any mortgage decision, on the basis of the information, read here. Similarly, if you see a financial or tax strategy, discussed here, please consult a licensed and qualified investments or tax advisor to ensure that the strategy is right for you. Mortgages, investments, and tax strategies mentioned in this Web site are not suitable for all. In many cases, they may not ever be feasible or lead to serious risks. While reasonable efforts to ensure the accuracy of the information and data contained herein, accuracy, suitability, completeness, and facts cannot be guaranteed. Past performance is not good prognozator for future results. Results, percentages, strategies and conditions are not guaranteed, and THIS YEAR'S CMT MUSIC and associated takes no responsibility for any losses which may arise from your use of this information. The information on this site reflect purely our opinions and not necessarily the opinions of any other party. Readers are welcome to add comments. However, comments that are off topic, quarrelsome, accusatory without evidence, the hated Spanish insensitive, profane, libelous, misleading, made under different names by the same IP address, or otherwise rude, or is deemed inappropriate from THIS YEAR'S CMT MUSIC, can be removed without notice. THIS YEAR'S CMT MUSIC news site and is not related to most of the people or companies. Company logos and trademarks shown here are the property of their respective owners, are displayed only for comment, are not intended to be used in a competitive way with the owner and should not imply an association or affiliation between THIS YEAR'S CMT MUSIC and said brand owner or its products or services. Information here is not intended to be nor represent him, mortgage advice, investment advice, tax advice, financial advice, recommendations or have indicated for the purchase or sale of securities. THIS YEAR'S CMT MUSIC personnel and affiliates may have an interest in mortgages, services, companies, products or securities on this site. Contact us if you require clarification of the above. THIS YEAR'S CMT MUSIC is owned and operated by McLister enterprises Inc. For questions about the news to see here, mortgages, copyrights, or republishing'S CMT MUSIC content, contact us at (800) 280-2460 or info@canadianmortgagetrends.com. Thank you for reading THIS YEAR'S CMT MUSIC. Copyright 2010. All rights are reserved.

Loans for people on debt management

- Credit loans: the immediate decision, no fee- image ProfessionalCashAdvance

You have a debt management program and are looking for a loan with bad credit institutions. Here are some of the lenders that offer same day loan no credit limit check.

If you have entered a debt management program, this is a registered credit reference agencies. If you do, don't waste the approver to the banks of the applicable period of time. The amounts secured by way of an unsecured cash loans or debt management are available in respect of the human is not a credit check box, but you need to think outside the box.

I would like to assess customer credit lenders, so the lack of credit scoring, which means that the credit cost is higher. Consumers Union stated: "in the interest of such transactions are awesome 212% of the one-month loan." Even if you can provide default security, you are more likely to be in such a way as to reflect the actual annual interest rate risk.

To approve the credit loans

Provided that for the approver signature loans bad credit history, as the case may be, for not more than 3 000 lenders for bad credit are available. The person who cosigns the loan is usually a very close friend or family member with very good credit Score.

If you are in default of a credit agreement, you shall be responsible for the repayment of the debt of the approver. Because of the amount of the interest rate and the advance pertaining thereto in respect of the Kingdom, this is a very important aspect. The Federal Trade Commission (FTC) offers some useful advice on the selection you then make in the exercise of the loan.

Family loans

If the family member is ready, it's a good idea to ask for a loan, the signs client if they are willing to lend money. The main advantage is that you pay much less interest. Taking into account the fact that most bad credit rating in each of the loans, the cost of $ 25 to $ 100 you borrow, you might want to check, if you are ready to help.

Borrowing money from a family member has its pitfalls. If you are unable to pay the debt, it could put a strain on your relationship. Do not haudata your head, talk about them and Sandy explains what has happened. They may be ready to provide the repayment holiday.

Pawn Shop loans

The value of the loan item, Pawnbrokers people, such as gold and jewellery. How much of your own security, it should be borne in mind and is ready to lend you up to 50% of the value of the assessment. As long as you can provide identity, it does not matter if the worker or the bank account.

Pawnbroker lending is protected in such a way as to avoid the failure to pay will result in forfeiture of your own. It is therefore not suitable for use, which is held by the sentimental value of the classification. However, if you can pay the interest that accrues, you may be able to extend the agreement for a month.

Payday Loans cash advance

Provided that you are a full-time employee, you may need up to $ 1000 without any guarantees for the loan. A citizen of the United States, over 18, has its own bank account and shall be submitted to the lender, there are two types of identification. Although it can be used to extend the lending term, income tax is one calendar month.

The advance in the Small loan is not available in the United States, including Georgia, Virginia and Ohio. Other States may have been the maximum restrictions that may lend and the rate. For example, the California borrowing limit is only $ 300.

Loans for people on debt management

Taking into account the obligations of credit institutions manage debt solution for you, I think very carefully before borrowing any extra cash. You have found it difficult to manage the credit agreements in the past, and entered the economic equilibrium of its own to restore the debt management program. Do you want to aggravate economic difficulties?

A poor credit history loan is not Cheap, so making the repayments are likely to jeopardize the future of their own ability to meet the expenses for the month. Do not use to make frivolous shopping, managing only to real money. Don't just leave the money in the foreign.

The Sources Of The

sábado, 7 de mayo de 2011

MBS REMINDER: 5/6/2011

Afternoon market updates

* US MARCH CONSUMER CREDIT RISES to $ 6.02 TRILLION (CONSENSUS RISE $ 5.0 TRILLION) VS REVISED $ 7.55 TRILLION INCREASE EFFICIENCY in FEB * USA MARCH CREDIT INCREASES $ 1.95 TRILLION VS. $ 2.60 TRILLION DECREASE in FEB; MARCH is NOT the CREDIT is $ 4.07 TRILLION VS $ 10.15 TRILLION INCREASE in FEBRUARY

Is a little surreal, but tens are 3.146 at the moment and FNCL 4.5 are up to 3 of 103 ticks-18, both better than yesterday's best characters. Already visible reprices on better, but a larger majority of lenders should get on board with the most recent movements. Despite the refusal with the Greek Minister of finance, on rumors Greek dropout of the EU, in conjunction with the inventory of a gear lever, technicals and fundamental concerns about the pace of recovery are fueling bond-bullishness/stock weakness.

* RTRS-11: 54-the GREEK GOVERNMENT HAS RAISED the POSSIBILITY of LEAVING the EURO AREA and re-establishing ITS OWN CURRENCY-GERMANY, SPIEGEL ONLINE * RTRS-11: 55-SPIEGEL ONLINE SAYS FIN MIN FROM the EURO area and the EUROPEAN UNION COMMISSION HOLDING a CRISIS meeting in LUXEMBOURG on Friday EVENING * RTRS-11: 56-SPIEGEL ONLINE SAYS MEETING AGENDA INCLUDES the POSSIBLE DISLOCATION DEBT RESTRUCTURING for GREECE * RTRS-11: 57-SPIEGEL ONLINE SAYS GERMANY is FIRMLY AGAINST GREECE for ANY DISCUSSION to LEAVE EUROZONE * RTRS-12: 09-GERMANY GOVT SOURCE SAYS THERE are NO PLANS for GREECE to LEAVE EUROZONE * RTRS-12: 38-the SOURCE of the EURO AREA: SOME MINISTERS are meeting in LUXEMBOURG to REVIEW ISSUES INCLUDING PORTUGAL, GRECJADZIEDZICZENIA THE ECB BUT NOTHING MORE

Speculation that Greece is considering leaving the EU and re-establishing its own currency is cited as a potential cause of the latest mini-sell-off in stocks and a rally in TSYs. The said rally leaves 10-yr notes on 3 182, best levels from the focal points of the Reitox network. But the better story is in the MBS where FNCL 4.5 only selected to the Cape, 1 scale up on the 103-15, at reprices on better possibility.